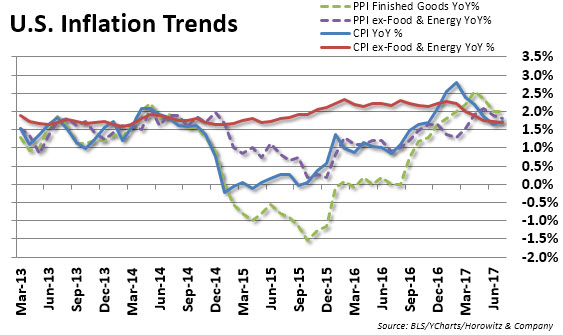

The question on the minds of many is whether or not the Federal Reserve can hikes rates again this year. The latest inflation report may put a kibosh on that thought for a while. While the Fed has set a 2% yearly inflation target, the latest Consumer Price Index rose only 0.1% in July. On a year-over-year basis, it fell short of the Fed’s goal coming in at a 1.7% gain.

Core consumer prices rose 0.1% for a fourth consecutive month in July, so annualized core inflation also posted a gain of 1.7%. The Producer Price Index fell 0.1% last month; analysts polled expected a 0.2% rise.

The good news is that with more than 90% of companies in the S&P 500 reporting for the second quarter, results have been impressive. FactSet now projects a blended earnings growth rate of 10.2% for the S&P 500 for the second quarter, along with a 5.1% blended sales growth rate.

S&P component firms that generated less than 50% of their sales outside the U.S. are set to record 14.0% blended earnings growth and 6.0% blended revenue growth.

At Friday’s close, gold hit a 2-month high of $1,294.00 as political tensions were on the rise. In fact, gold gained a whopping 2.3% for the week. Some of that has since been reversed as markets are not as jittery since the North Korea rhetoric has subsided – for now.

Last week the Dow Jones Industrial Average declined 1.06% to 21,858.32; the S&P 500, 1.43% to 2,441.32; the Nasdaq Composite, 1.50% to 6,256.56. Volatility certainly came back as the CBOE VIX jumped 53.44% to end the week at 15.39 (now dropping to 12.50)

Key reports this week:

On Monday, Cumulus Media and Sysco report quarterly results.

Tuesday we will see July retail sales numbers and earnings from Advance Auto Parts, Agilent, Coach, Dick’s Sporting Goods, Home Depot, TJX, and Urban Outfitters.

On Wednesday, minutes from the July Federal Reserve policy meeting appear; Wall Street will also interpret a report on July housing starts and building permits and earnings news from Cisco, L Brands, NetApp, Stein Mart, and Target.

Thursday brings reports on initial jobless claims and industrial production. Earnings from from Alibaba Group, America’s Car-Mart, Applied Materials, Bon-Ton Stores, Gap, Ross Stores, Sportsman’s Warehouse, Stage Stores, and Walmart are also on tap.

Friday, investors will gain insight on earnings from Deere & Co. and Estee Lauder and the preliminary August consumer sentiment index from the University of Michigan.

{kind=link}