Hope, Fear – Where Are We In the Cycle?

It was a brutal quarter for equities. The full-year was not too pretty either. In fact, looking back, it was one of only a few times in history that all major asset classes closed lower for a calendar year. In other words, there were very few places to hide from the storm that approached quietly and then rained down with a vengeance during the final quarter.

Throughout the year there were various issues and unknowns that had arisen causing a culmination of disparate matters setting the stage for what occurred. Some of these were well known and others less apparent. Trade-wars, slowing global growth, rising interest rates and then a government shutdown all attributed to the ultimate breaking point.

Quite a bit of excitement surrounding the benefit of tax cuts came at the beginning of the year. This allowed for a boost in corporate earnings, as well as consumer confidence, which helped equities shake off some of the other issues the economy faced. This benefit, however, appears to be dissipating and outweighed by the ever-growing list of concerns that need to be resolved. Even as the tax cuts help to keep earnings growth positive for the near-term, the forward trajectory of that growth is slowing. Investors initially got ahead of themselves, not thinking about how this would eventually play out. This is nothing new as market psychology often shows a bout of euphoria before depression sets in. It is a cycle that repeats itself over and over.

The question that we are looking to answer is simple: Where are we now in the cycle? Did the recent market sell-off provide enough of a shake-out to provide evidence of a capitulation? Was there enough pain inflicted that the cycle bottomed and there is a renewed optimism ahead? Are there still unresolved issues that need to be addressed prior to moving forward?

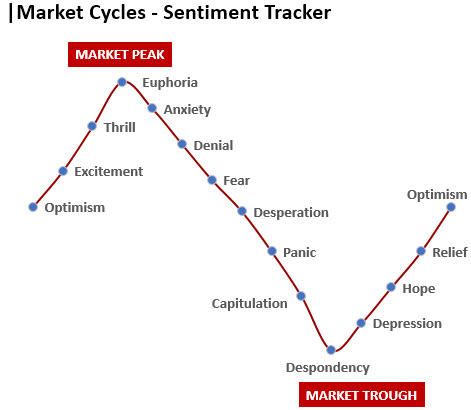

Looking at the S-curve of market sentiment, we can notice that there are several waves that form over time. From peak to trough and back again. Optimism turns into euphoria at market peaks and then fear eventually breaks toward despondency at market troughs. Depending on your vantage point, one can make an argument about what best describes the current investor sentiment. If you are of the bearish persuasion, it probably looks as though it is somewhere between anxiety and denial. Bulls could argue that sentiment is leaning toward the level of hope or possibly relief.

Looking at this on a market basis, we clearly saw a peak in 2018 that led to anxiety and maybe even a few bouts of desperation or panic. From an individual stock perspective, many have gone through an entire cycle recently as prices have swung from historic highs and now are off of those levels by 30% or more. While there is no scientific method to exactly pinpoint the current level of sentiment or the future direction, it is important to understand that investor behavior and psychology are key components of market pricing.

Confidence in the outlook and the ability to assign risk to an investment helps provide a reasonable expectation for the future. Lacking that confidence leads to confusion and risk avoidance. That brings us right up to the present, where the current environment is not helping to create a solid base of certainty. As a perfect example, we are seeing many companies nixing forward guidance and explaining that they have limited ability to project out what their business will look like over the next few months. That is disconcerting and investors will be hard-pressed to bring up any amount of excitement with that as a backdrop. Until there is more clarity, it would appear as though markets will be rangebound, only able to break out (up or down) once there is a better ability for investors to calculate a reasonable level of risk and reward.

Over the past several months, these factors have guided us to more frequently update and rebalance portfolios. This is part of the ongoing process as we look to bring portfolios in line with the positioning that fits our forward economic outlook. Essentially this process looks to rotate into positions/sectors that have been out of favor from those that have outperformed. The idea is to keep portfolios aligned with a specific risk model, time horizon and our global outlook.

“It is the set of the sails, not the direction of the wind that determines which way we will go.“

– Jim Rohn

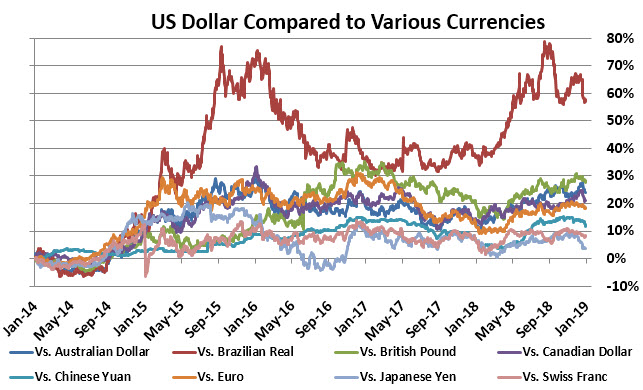

With that in mind, we have made incremental updates to our outlook for the global economy. As 2019 approached, we have been keenly aware of the rising U.S. Dollar. This has negatively impacted foreign and emerging markets for some time. As mentioned, we also believe that a good chunk of the earnings growth for U.S. equities appears to have reached a peak as the benefits from the tax cuts fade.

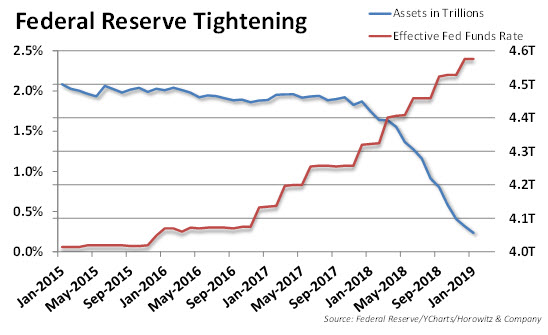

We also recognize that the Fed has been on a tightening path for the past two years. If history is any guide, we know that it takes some time for rate hikes and Fed tightening programs to start to show results. The past rate hikes and monthly reductions of the balance sheet (normalization track) are now taking hold as liquidity is being drained from markets. So far, the Fed has been holding on to their belief that a progression of their tightening program is warranted. This is in the face of an obvious global slowdown that may make its way to the U.S. in the near future. The truth is that no country is an island as the world’s economies are so tightly interconnected.

However, if the economic backdrop for the U.S. begins to slow, we would expect the Fed to change, or at least adjust, the stance on their rate hike plans. The outsized deficit and ballooning debt could also come into play over the next year. Both of these issues have the capacity of causing the U.S. Dollar to weaken substantially – potentially benefiting foreign and emerging markets.

Another area that we have been watching closely is related to the credit markets. There have been signs that there are some pricing concerns on the lower end of the credit quality scale. This often occurs during market sell-offs and when economic conditions deteriorate. As investors have been reaching for yield over the past years, they have looked to lower-rated issues to provide opportunity. Some of the excessive buying is starting to unwind as concerns grow over the economic outlook.

These worries have been amplified by the recent predictions appearing in headlines that a recession is conceivable within the next two-years. Many of these prognostications are technically driven. They are considering the power of the economic cycle being front-loaded and then projecting that impact over time. Essentially, this is a nod to our previous 4th Quarter Economic Commentary titled “Cycles Pulled Forward” or the Pull Forward Effect thesis embodied by the analyst community.

Our early response was to adjust the allocation within the fixed income sector to increase credit quality while keeping duration on the shorter end of the spectrum. Over the course of the past few months, portfolios have generally seen a reduction in Floating Rate Bond exposure and an increase to higher quality, and shorter-duration bonds.

Foreign bond positioning has also seen a change. We have tilted the foreign bond exposure from U.S. Dollar hedged to unhedged – in line with our expectations that the appreciation for the U.S. Dollar has reached a peak.

After some serious review, we have added a new manager to the commodity sector as we had been disappointed in the performance and strategy execution of the previous two managers. At the same time, we have started the discussion of reducing the allocation or removing commodities altogether from portfolios. This may take some time to work through as we have an understanding of the benefits in utilizing uncorrelated assets within portfolios over longer time-frames. While we have always maintained a relatively low allocation to commodities, the space has become increasingly difficult to capitalize upon. Inflation has remained extremely tame and that fact seems to be the new normal. Technology, greater efficiencies in business and an extremely proactive Federal Reserve have kept inflation at bay, at least domestically, which has stymied growth in the commodity space. Even so, the continued underperformance of this specific sector is disconcerting and all options are being considered.

Effectively with these changes/updates, we are looking to get ahead of the curve a bit as we are seeing some interesting opportunities that may develop over the next year. At the same time, we are being careful to keep risk within appropriate ranges for each portfolio model allocation as markets enter a corrective mode for the time being.

(It is important to note that client portfolios may have differing levels of risk. Some or all of the above changes and updates may have been implemented and others not, depending on risk, time horizon and other specific portfolio considerations.)

Trade-War Update

Let’s all admit that this is getting really tiresome. The continuing rhetoric from both the U.S. and China is creating a worrisome backdrop for investors. If there is anything that we know, it is that markets hate uncertainty. Unfortunately, the reality is that this trade-war process is the poster-child for lack of confidence.

Companies are holding back on new initiatives, buyers are confused, manufacturing is going through a difficult stretch and the outward view is, at best, hazy. There is no way to quantify the impact as there are too many moving parts to consider. Essentially, when nothing is certain, anything is possible.

Take the latest report from China as a prime example. Most would have thought that the heavy tariffs on goods from China would have put a dent on imports. Yet, China reported a record trade surplus with the U.S. in 2018. Yes, this is in spite of the tariffs and trade-war. The official report shows a remarkable gap of over $320 billion of goods exported to the U.S. over imports.

You can be sure that this will get the attention of those that want to even the playing field. As we know, a good part of this may be attributable to front-loading as firms stocked up ahead of the tariff implementation. Still, the excessive amount of the surplus will not go unpunished and could cause for a further push to accelerate talks and plans to hit China even harder if there is no resolution by the March deadline.

Ironically, this will probably add to the push to import more products ahead of that deadline, thereby causing an even bigger surplus over the next few months. After that is where the problem lies. Even if there is a full resolution and both sides agree to play nice, imports may drop off of a cliff as many companies have filled their inventories in advance. This is a dangerous game as the potential for a significant slowdown in the future could create a panic as economic reports could paint a very ugly picture in the coming months.

{kind=link}