The end of the year is finally here and what a wild year it was. Starting off with a significant swoon at the beginning, 2016 ended with a massive post-election rally. The Fed was accomodative throughout and only raised rates once, even though they had projected four hikes.

Disregarding all of the geopolitical risk that was seen over the past year, investors still viewed equities, particularly in the U.S., as the place to be. As companies have been borrowing massive amounts to buyback stock and boost dividends, investor’s desire for yield has been insatiable.

As some of the euphoria over the hoped-for fiscal stimulus fade, valuations will surely need to be revisited. According to Factset, the forward 12-month P/E ratio is now 17.1, which is above the 5-year average and the 10-year average.

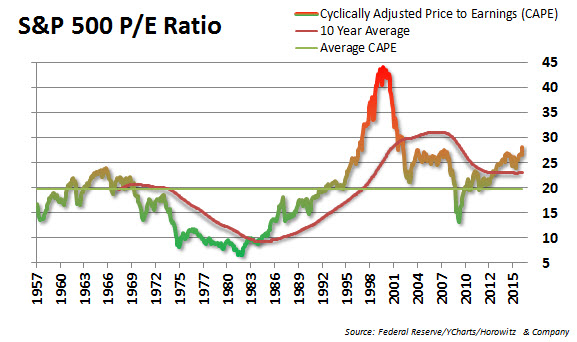

Looking at the chart of the CAPE P/E ratio (cyclically adjusted price-to-earnings ratio), we can see that the valuations appear stretched. In fact, the current CAPE P/E ratio is now the highest it has been since 2002 and just surpassed the 2007 levels.

The cyclically adjusted price-to-earnings ratio, commonly known as CAPE, Shiller P/E, or P/E 10 ratio, is a valuation measure usually applied to the US S&P 500 equity market. It is defined as price divided by the average of ten years of earnings (Moving average), adjusted for inflation.

As we have seen in the past, valuations can remain elevated for some time. As expectations rise, so does investor confidence. That is not a problem until it is a problem. In other words, if reality does not catch up to expectations there will eventually be a reversion to the longer-term averages.

The consensus opinion is that low interest rates allow for P/E expansion and that has some truth to it. However, we also know that markets are cyclical and any imbalance is corrected eventually.

Looking to 2017, there is some cause to be worried that excess valuations may become a detractor if the U.S. dollar strength continues. As tech has rallied with the market, the concern that the sector receives 58% of their revenue internationally may be something that becomes a serious headwind. Moreover, as many companies within the tech had issued impressive upside guidance last quarter, shares could be vulnerable into 2017. The Tech sector is not alone, Energy (43%) and Materials (49%) also have high levels of international revenue streams. On the other end of the spectrum, Telecom (3%) and Utility (6%) companies within the S&P 500 have the least international exposure.

One more thing: Tax considerations may have delayed selling in 2016 in order to reap the benefits of potential for tax cuts in 2017. If that is true, January may be a challenging month for equities. The bottom line is that with valuations at cautionary levels and many of the global growth and geopolitical risks unresolved, it pays to be cautious into the new year.

{kind=link}