As discussed in our previous quarterly, there is a cycle and relation of Fed Action and the economy. We discussed how we may be moving from a dovish fed and stronger economy to a more hawkish fed with also a stronger economy. As economic data continues to improve, this change in Fed sentiment may come quicker than many expect. Here is what we said previously:

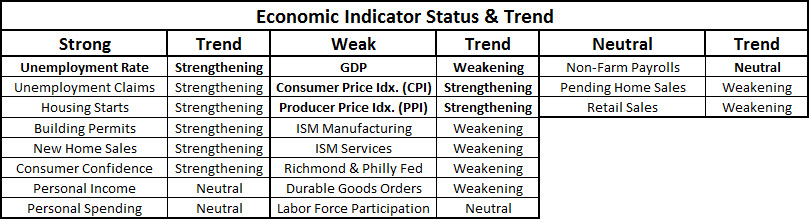

The changing tide from a Dovish Fed & Weaker Macro to a Dovish Fed & Stronger Macro may, over time, slowly switch to a Hawkish Fed & Stronger Macro. We believe that it is highly unlikely the Fed will become completely hawkish as the rate of inflation has still yet to cause any concern (CPI just over 2.0%). Moreover, a stronger macro environment is still some time away when considering some of the more recent economic indicators. Below is a table showing weak, strong and neutral economic indicators as well as their current trend. When we begin to see a few of these turn, we can then consider the macroeconomic environment to be strong/ strengthening, especially those in bold.

Here is how things looked at the end of the 3rd Quarter in 2016:

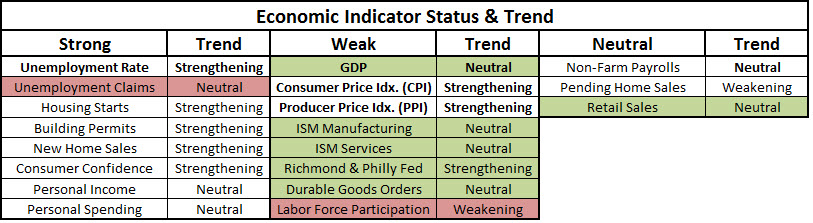

Here is how we believe things look now (Changes Highlighted in Green Improved and those Highlighted in Red Deteriorated):

While some of the indicators in the Weak column have started to improve, they are not yet strong indications of a heated or overheated economy. The Fed should be able to remain dovish until indications of GDP, Inflation and other indicators in the weak column move toward the strong column.

{kind=link}