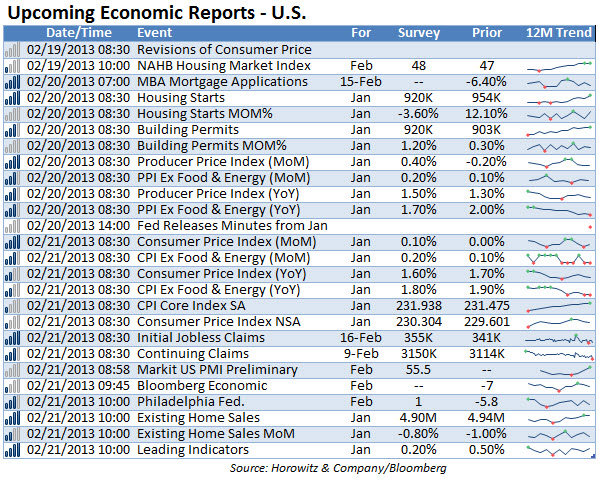

If nothing else, it is getting a bit more interesting out there. Aside from the same-old, same-old that we have seen thus far in 2013, there is some chatter that housing numbers will start to slow their recent recovery ascent. CPI and PPI (ex food and energy) should be benign, although the there are a few wildcards that could push these both a bit. If we look at the core, there will probably be a bump as the price of oil and gas have risen.

The mid-week focus will be on the Fed minutes. The last meeting may have seen additional concerns raised about the continuation of a zero interest rate policy (ZIRP) and/or the Fed’s QE program. Already we have been treated to several Fed governors that have been talking their book as part of the new and improved communication facility by the Fed.

(We discuss the market outlook in this week’s TDI podcast – Listen)

Leading indicators will finish of the week with a whimper. No one really seems to be paying too much attention to that number lately.

Clearly the dominate force that will be moving markets over the next couple of weeks will be the “final” outcome of the postpones fiscal cliff plan. As of now, there does not seem to be anyway that a deal of any sort will be reached and the automatic cuts will go into effect. However, as we have seen in the past, this administration and Congress excel at making one particular decision regularly: postponement of any decision.