Bloomberg Columnist David Powell had some interesting thoughts on the Euro area and Euro. Over the past two days, the Euro is up just about 2%, which is pretty remarkable. (more info on Bloomberg Briefs)

From Powell:

ECB President Mario Draghi indicated the Governing Council is unlikely to ease monetary policy in the first quarter. Economic weakness would probably have to persist until the second quarter for an additional reduction of interest rates.The hawks have taken control of the Governing Council. Draghi said the decision to leave interest rates unchanged was unanimous. He added: “if the decision was unanimous, it implies that there was no request to have a rate cut.

One thing implies the other.” The president‘s tone was more dovish yesterday than in December. last month, he said: “There was a wide discussion (about interest-rate cuts) but in the end the prevailing consensus was to leave the rates unchanged.”An acknowledgment of the interest rate on the deposit facility possibly being pushed into negative territory added to the dovishness of his tone in December. “We are operationally ready (for a negative interest rate on the deposit facility) but the discussion didn‘t go into any depth with respect to this point,” he stated. “We briefly touched upon the complexities that such a measure would involve and the possible unintended consequences but we didn‘t elaborate any further.”A Bloomberg News story {“majority of ECB Governing Council Said to Support rate Cut.” Dec. 7, 2012.} later confirmed a majority of the Governing Council wanted to reduce the main policy rate in December. The move was reportedly blocked by Draghi and Executive Board members Benoit Coeure and Jörg Asmussen and Bundesbank President Jens Weidmann.

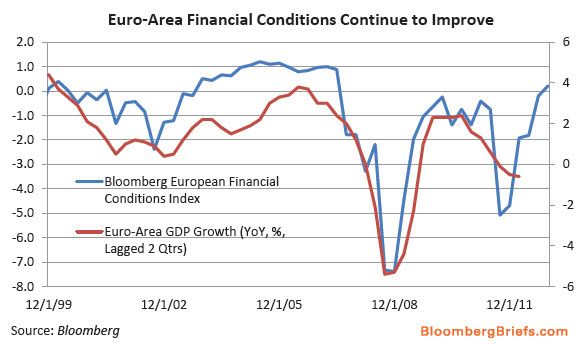

Draghi yesterday said the improvement in financial conditions and the stabilization of some surveys would probably lead to an increase in real economic activity. “if you look at what‘s happening in the last six months, you will see a significant improvement in financial market conditions and a broad stabilization of some conjectural indicators,” he stated.The Bloomberg Euro-Area Financial Conditions index confirms his statement. it has risen to 0.5 from a recent low of minus 2.4 in June. The index combines yield spreads from the bond and money markets and readings on the performance of equity markets into a normalized index. it is expressed in terms of a z-score, which is a measure of the number of standard deviations from the long-term mean. The period of the average is from 1999 to 2008. {FCON }The index has a lead time of two quarters.

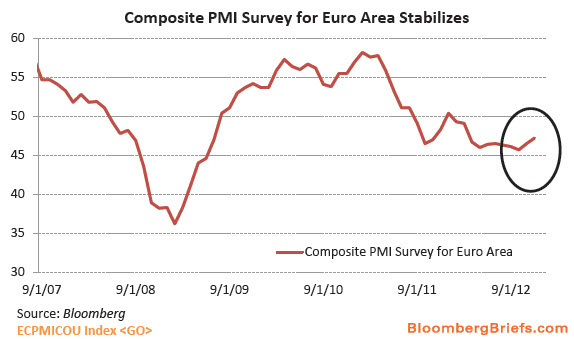

The quarterly correlation between the index – with a two-quarter lead – and year-over-year GDP growth from the first quarter of 1999 to the fourth quarter of 2010 stands at 0.86. The PMI surveys for the euro area have shown some stabilization, though they fall short of signalling a recovery. The composite reading rose to 47.2 in December from 46.5 in November and a recent low of 45.7 in October.

Economists generally require three consecutive moves in a new direction to declare a change of trend.Calls for monetary easing from the doves may return in the spring if the improvement in the above-mentioned economic indicators fails to indicate an increase in output in the second quarter. GDP fell 0.2 percent between April and June and 0.1 percent between July and September. The PMI surveys suggest output may have shrunk again in the fourth quarter.