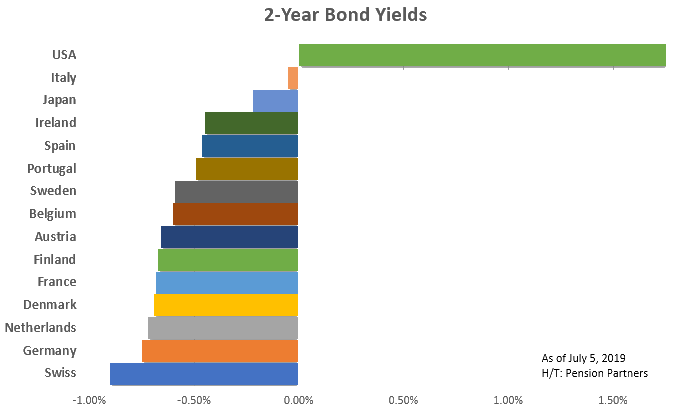

Many have questioned why there is the potential for a rate cut if the U.S. economy is holding up well in the face of a global slowdown. On the heels of a “pivot” by the Fed in late 2018, the yield on the 2-year US Treasury has slipped from 2.95% to 1.75%. By any measure that is a noteworthy move in a relatively short period of time.

The real concern is that the yield curve is inverted and that is not beneficial to the U.S. economy over time. But what we have discovered is that the curve inversion may not be due to anything related to the U.S. economy at all. Let’s explain…

A big part of the reason for the drop in yields can be credited to the notion that the Fed is no longer looking at hiking rates and is now embarking on an easing program. Investors are reassessing the outlook and have been buying bonds ahead of any potential rate cut.

There is also another reason. Something that is at work behind the scenes.

Essentially there is the potential for a global bond arbitrage that is going on.

With bond yields showing negative yields for sovereign debt, governments are issuing bonds at a record rate and reinvesting the proceeds into U.S. Treasuries.

Here is how it works:

Let’s look at Germany as an example. The government is issuing 2-year notes at a negative yield of -0.75% per year. The European Central Bank (ECB) is purchasing that debt through their quantitative easing program. Germany, (the issuer of the bond) is destined to make money on the transaction since every $100,000 issued/bought, will return $98,500 to the ECB. In other words, the ECB will lose $1,500 on the transaction and the German government will benefit by $1,500 over the 2-year period.

What does Germany do with the money it takes in from the bond sale? They could use the funds to improve their local economies or infrastructure. Or, they could easily take it and match the term of the issue and purchase a 2-year U.S. Treasury. This will essentially guarantee a return of 1.75% per year, assuming they hold the bond until maturity.

The outcome of this guaranteed arbitrage is a total gain of 5.00% on their bond issue. Not a bad deal as there is very little risk and the negative yield loss is assumed by another party. Currency risk plays a role in this, but this can be partially hedged out or potentially manipulated to benefit the country buying the U.S. bonds. Naturally, hedging costs will reduce the benefit of the strategy.

Looking at this another way, we must understand that the longer rates stay in negative territory for countries outside the U.S., the more impact it will continue to have on the yields of U.S. Treasuries. Countries with negative yielding debt are natural buyers of U.S. Treasuries as there is limited risk associated with the opportunity. Even if the Fed wanted or needed to raise rates, U.S. yields will remain artificially low as the ECB (and other countries with negative yielding debt) continue to provide funding for buying positive yielding debt on a favorable basis.

{kind=link}