There is creativity and then there is desperation. The real question these days is finding that fine line and recognizing the difference.

The FED and the financial powers has thus far been classified as creative in their “handling” of the credit crisis. Yesterday, during a very exciting (?) testimony from Fed Chief Bernanke, a news item flashed across the wire that Fannie Mae (FNM) and Freddie Mac (FRE) will reduce the spread caps, thus allowing for additional capital and credit to flow into the economy.

The timing of the OFHEO announcement is at best suspicious and very worrisome. It came too close to the discussion by the FED about their understanding that there is a significant housing problem and there are more problems projected. There is clearly a need for additional capital directed towards consumers who are in a credit stranglehold. Yet, this seems to be more of a desperate move and a gamble on the future security of the credit markets. Remember, the reason why there were caps in the first place:

From the OFHEO: Since agreements reached in early 2004, OFHEO has had an ongoing requirement on each Enterprise to maintain a capital level at least 30 percent above the statutory minimum capital requirement because of the financial and operational uncertainties associated with their past problems. In retrospect, this OFHEO-directed capital requirement, coupled with their large preferred stock offerings means that they are in a much better capital position to deal with today‘s difficult and volatile market conditions and their significant losses.

Excuse me, but a release of the cap will help to keep their problems in check? Surely there are different problems now and the 30% cushion helps to keep the stability of the quasi-agency companies during times when write-offs and write-downs are growing. The cushion is analogous to the loan-to-value that homeowners are required to have as they buy their homes.

One of the problems that helped to enhance the mess that we find ourselves in was the lack of a belief that old-fashioned loan and risk management procedures were of no consequence. Bad assumptions were/are standard operating procedure (SOP) and we now know that it was not the best way to operate.

— Andrew’s Book – The Disciplined Investor is available at Amazon and other fine retailers —

So, when markets are elated with the news that the CAP cushions are going to be lifted with FNM and FRE, don’t be upset when you see a continuation of massive losses. Rest assured they will continue to flow like a raging river for some time to come.

Why? Here are some of the headlines into this brilliant plan:

– Freddie Mac Posts Wider Loss of $2.5B in 4th-Qtr As Loan Defaults Mounted

– Big loss for Freddie Mac

– Fannie Mae posts nearly $3.6B loss in 4Q

– Moody’s Warns ‘Sizable’ Losses May Be Ahead for Fannie Mae

– Moody’s puts Fannie Mae rating on review

– Freddie Mac posts wider loss of $2.5B in 4th-qtr as loan defaults

The fact that Moody’s is looking into downgrading these names is one of the few murmurs of sanity that can be separated from much of the rhetoric that is being bantered about. It is clear that the companies that are in dire need of credit expansion (builders, retailers) may be acting on a last-ditch-effort approach that will have them spin positive on any plan, no matter how detrimental it will be to our financial health.

Briefing.com noted on FRE: The company’s estimated regulatory core capital was $37.9 billion at the end of 2007, $3.5 billion in excess of the 30% mandatory target capital surplus directed by OFHEO.

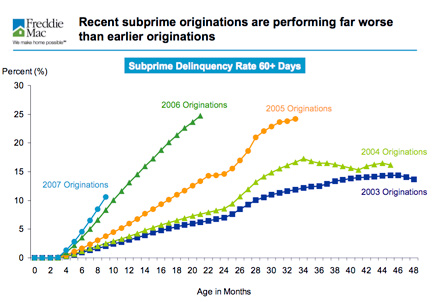

The core capital may seem like a substantial number at first glance but put that into perspective against the backdrop of an estimated mortgage portfolio of $1.8 trillion. In addition, the losses that have been reported for 2007 are more than they have experienced in the last 7 years. FRE is also reporting that the average current adjusted loan-to-value ratio for their single-family home portfolio has been increasing steadily over the past few years. It now is 60%, up from a low of 56% in 2005.

Even so, they have 16% of subprime ARM loans that are 90-days or more delinquent or now in foreclosure. This is far greater than any time over the past 10-years. ARMs are considered Hybrid Mortgages and as this category currently makes up 17% of their portfolio, there is reason to be cautious.

As housing prices continue to decline, loan-to-value ratios will continue to suffer. This is just one more part of the larger concern that investors will have to ingest as they are asked to commit more funds in the form of debt and preferred stock offerings. In the face of a credit rating panic, it will be interesting to see how they adjust their portfolio strategy to ensure that investors see the highest rating available in order to efficiently peddle their debt at the lowest cost.

Either way, FRE and FNM will surely have a higher cost of operations as they move forward. Everything points to lower net earnings and higher investor anxiety.

Chronic borrowers will be excited as there will, in theory, be more of the credit-drug available to help get them deeper into a their debt-hole. But do not make the mistake as an investor that it may be time to jump in. This move will have a negative effect and eventually weakening FNM and FRE. Simply using debt-to-equity ratios as a proxy for loan-to-value will show that this is more of a creative mechanism for credit to flow that will have the near-term effect of throwing these two companies under the bus.

We have no change to our outlook for these companies (see Mortgage Mayhem 11/21/07) and continue to warn investors that this type of gamble may lead to further solvency issues rather than balance sheet stability. Any downgrade (hard to fathom?) will also create a greater problem as the cost for asset-backed credit will eventually be need to be paid by….you and me! These will take the form of a tax burden that will be left to be cleaned up by the “winners” of the upcoming election.

The bottom line: FRE and FNM are being thrown under the bus in order to help the housing markets and in an effort to protect the credit markets. The removal of the mandatory CAP is a dangerous gamble by regulators. There is not much to say from a technical standpoint either. In the end, there needs to be a sacrifice to save the rest of us. FRE and FNM may well be the burnt-offerings to appease the credit gods.

FNM 1-Year Chart

FRE 1-Year Chart

Disclosure: Horowitz & Company Clients do not hold positions in any securities mentioned as of the date of publication

Subscribe to The Disciplined Investor Podcast – great guests and great investing ideas !