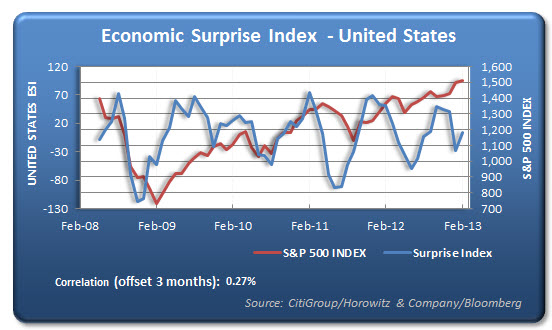

Often times, economics are a big part of the reason for stocks and markets to move. Of course, earnings are important as well. However, with central banks continuing to provide extreme liquidity, neither of these will have as much weight since no matter what the outcome, there is always the hope that the Fed will come to the rescue.

I thought we would take a quick look at the Eco Surprise Index and compare that to the S&P 500. Of late, there has been a mixed bag of surprises to the upside and downside. But looking back to January, there was clearly a bit more “better” surprises that helped to provide investors with more reason to buy. When economists are too low with their estimates, they often ratchet up the their future expectation and that is what we are seeing now and the most recent reports have been disappointing.

The Citigroup Economic Surprise Indices are objective and quantitative measures of economic news. They are defined as weighted historical standard deviations of data surprises (actual releases vs Bloomberg survey median). A positive reading of the Economic Surprise Index suggests that economic releases have on balance been beating consensus.

The indices are calculated daily in a rolling three-month window.The weights of economic indicators are derived from relative high-frequency spot FX impacts of 1 standard deviation data surprises. The indices also employ a time decay function to replicate the limited memory of markets.

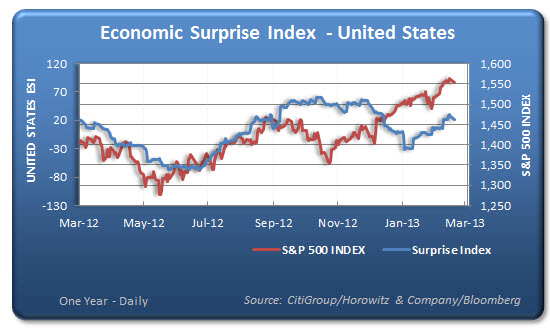

– A longer term view –